Home Loan EMI Calculator – Complete Guide for Smart Home Buyers

Buying a home is one of the biggest financial decisions in life. Whether you are purchasing your first apartment, investing in property, or upgrading to a larger house, understanding your loan repayment is extremely important. This is where a Home LoanEMI Calculator becomes useful.

A home loan EMI calculator helps you estimate your monthly installment, total interest payable, loan eligibility, tax benefits, and even how much time you can save by paying one extra EMI every year.

What is a Home Loan EMI Calculator?

A Home Loan EMI Calculator is an online financial tool that helps borrowers calculate the monthly EMI (Equated Monthly Installment) payable towards a housing loan.

The calculator uses three important inputs:

- Loan Amount

- Interest Rate

- Loan Tenure

Based on these values, it instantly calculates:

- Monthly EMI

- Total Interest Payable

- Total Repayment Amount

This helps borrowers plan finances better before applying for a home loan.

Home Loan EMI Formula

The EMI for a home loan is calculated using the formula:

EMI = \frac{P \times R \times (1+R)^N}{((1+R)^N-1)}

Where:

- P = Principal Loan Amount

- R = Monthly Interest Rate

- N = Loan Tenure in Months

Although the formula looks complicated, online EMI calculators make it extremely easy to calculate instantly.

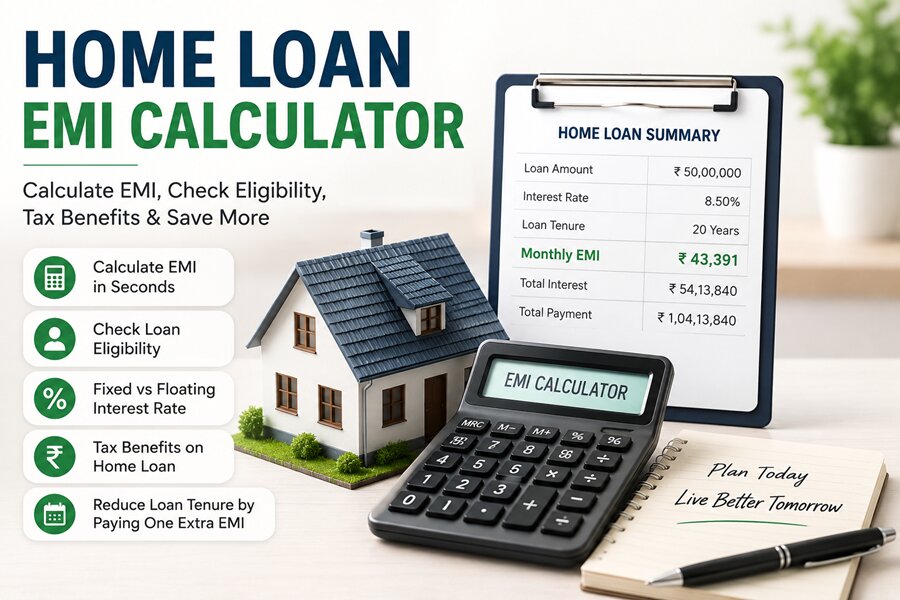

Example of Home Loan EMI Calculation

Suppose:

- Loan Amount = ₹50 Lakhs

- Interest Rate = 8.5%

- Loan Tenure = 20 Years

The approximate EMI will be:

- EMI = ₹43,391

- Total Interest = ₹54 Lakhs approx.

- Total Payment = ₹1.04 Crore approx.

This example shows how interest significantly increases total repayment over long tenures.

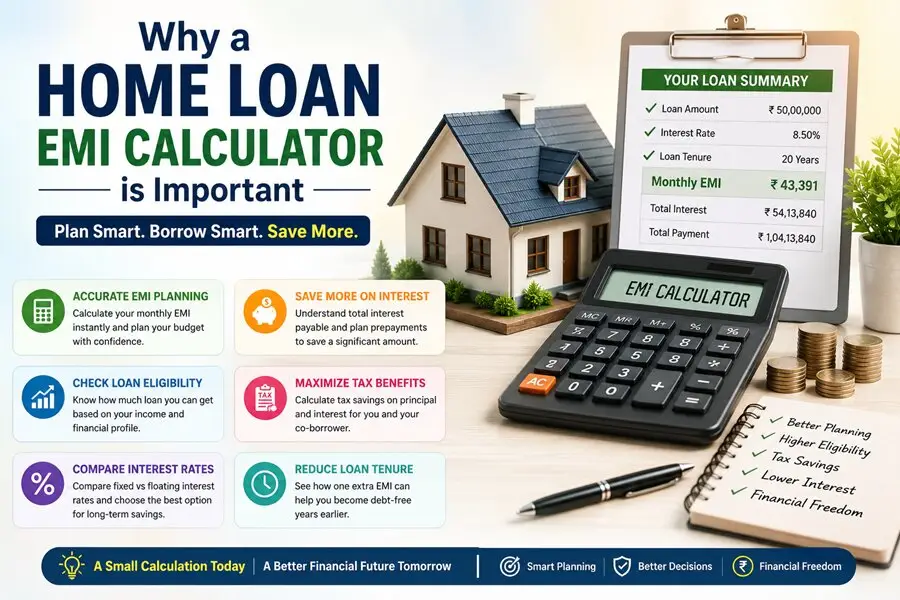

Benefits of Using a Home Loan EMI Calculator

1. Better Financial Planning: You can check whether the EMI comfortably fits your monthly budget.

2. Compare Loan Offers:Different banks offer different interest rates. EMI calculators help compare lenders easily.

3. Understand Interest Burden: You can estimate total interest payable before taking the loan.

4. Choose Ideal Loan Tenure: Longer tenures reduce EMI but increase total interest.

5. Improve Loan Eligibility: Understanding EMI calculations helps optimize the income-to-obligation ratio.

How Much Home Loan Can I Get on ₹1 Lakh Salary?

One of the most searched queries in India is:

“How much home loan can I get on 1 lakh salary?”

Most banks use the FOIR (Fixed Obligation to Income Ratio) to determine eligibility.

Typically:

- Banks allow 40% to 55% of monthly income towards EMIs.

- Existing loans and credit card dues also affect eligibility.

Estimated Home Loan Eligibility on ₹1 Lakh Salary

| Monthly Salary | Approx EMI Capacity | Estimated Loan Eligibility |

|---|---|---|

| ₹1,00,000 | ₹45,000 – ₹55,000 | ₹45 Lakhs – ₹70 Lakhs |

Factors Affecting Eligibility:

- Age

- Existing EMIs

- Credit Score

- Employer Type

- Loan Tenure

- Interest Rate

- Co-applicant Income

If you have no existing loans and maintain a strong credit score above 750, you may qualify for a higher loan amount.

Home Loan Eligibility Calculator Based on Income

A Home Loan Eligibility Calculatorestimates the maximum loan amount a person can borrow based on income and financial obligations.

Key Inputs in Eligibility Calculation

1. Monthly Income

Higher income improves eligibility.

2. Existing Liabilities

Car loans, personal loans, and credit card dues reduce eligibility.

3. Age

Younger applicants get longer repayment tenure.

4. Credit Score

A higher score improves approval chances and interest rates.

5. Loan Tenure

Longer tenure increases eligibility due to lower EMIs.

Salary vs Home Loan Eligibility Table:

| Monthly Income | Approx Home Loan Eligibility |

| ₹30,000 | ₹18 – ₹22 Lakhs |

| ₹50,000 | ₹30 – ₹40 Lakhs |

| ₹75,000 | ₹45 – ₹55 Lakhs |

| ₹1,00,000 | ₹55 – ₹70 Lakhs |

| ₹1,50,000 | ₹85 Lakhs – ₹1 Crore |

These figures vary based on bank policies and borrower profile.

Joint Home Loan Tax Benefit Calculator

A joint home loan allows two or more individuals to take a loan together. It is commonly taken by:

- Husband and Wife

- Parents and Children

- Siblings

The biggest advantage of a joint loan is higher tax savings.

Tax Benefits on Joint Home Loan

Under Indian Income Tax laws:

Section 80C

Deduction up to ₹1.5 Lakhs per co-borrower on principal repayment.

Section 24(b)

Deduction up to ₹2 Lakhs per co-borrower on interest payment.

Example of Joint Home Loan Tax Savings

Suppose:

- Husband and wife jointly pay a home loan.

- Annual interest = ₹3.5 Lakhs

- Principal repayment = ₹2 Lakhs

Potential combined tax benefits:

| Tax Section | Husband | Wife | Total Benefit |

| 80C | ₹1.5 Lakhs | ₹1.5 Lakhs | ₹3 Lakhs |

| 24(b) | ₹2 Lakhs | ₹1.5 Lakhs | ₹3.5 Lakhs |

This significantly reduces taxable income.

Fixed vs Floating Interest Rate Calculator

Choosing between fixed and floating interest rates is one of the biggest home loan decisions.

What is Fixed Interest Rate?

A fixed-rate home loan keeps the interest rate constant throughout the tenure.

Advantages

- Stable EMI

- Better budgeting

- Protection from rising rates

Disadvantages

- Usually higher than floating rates

- Limited benefit when rates fall

What is Floating Interest Rate?

A floating rate changes according to market conditions and RBI repo rate movements.

Advantages

- Lower starting rates

- Benefit when interest rates reduce

Disadvantages

- EMI may increase

- Less predictability

Fixed vs Floating Interest Rate Comparison

| Feature | Fixed Rate | Floating Rate |

| EMI Stability | High | Medium |

| Risk | Low | Moderate |

| Initial Interest Rate | Higher | Lower |

| Benefit During Rate Cuts | Now | Yes |

| Suitable For | Conservative borrowers | Long-term borrowers |

Which is Better – Fixed or Floating?

Choose Fixed Rate If:

- You want stable monthly payments

- Interest rates are expected to rise

- You prefer financial certainty

Choose Floating Rate If:

- You can handle EMI fluctuations

- Interest rates may reduce

- You want lower long-term costs

Currently, many Indian borrowers prefer floating-rate loans because they generally offer lower interest over long tenures.

How Many Years Can I Reduce by Paying One Extra EMI?

One of the smartest home loan repayment strategies is paying one extra EMI every year.

Even a small additional payment can significantly reduce your loan tenure and interest burden.

Example: One Extra EMI Every Year

Suppose:

- Loan Amount = ₹50 Lakhs

- Interest Rate = 8.5%

- Tenure = 20 Years

- EMI = ₹43,391

If you pay one extra EMI annually:

- Loan tenure may reduce by approximately 3 to 5 years

- Interest savings can exceed ₹10 Lakhs

Why Does This Strategy Works?

In the initial years:

- A large portion of EMI goes toward interest

- Small principal reductions create huge long-term savings

Extra payments directly reduce the outstanding principal.

Benefits of Paying One Extra EMI:

1. Faster Loan Closure: Become debt-free earlier.

2. Massive Interest Savings: Reduce total repayment amount significantly.

3. Improved Financial Freedom: Less long-term financial stress.

4. Better Credit Health: Faster repayment improves financial profile.

Tips to Reduce Home Loan EMI

1. Increase Down Payment: Higher down payment reduces loan amount and EMI.

2. Improve Credit Score: A score above 750 helps secure lower interest rates.

3. Choose Longer Tenure Carefully: Long tenure lowers EMI but increases interest.

4. Prepay Whenever Possible: Use bonuses and incentives for prepayments.

5. Balance Transfer Smartly: Shift loan to another bank if interest savings are substantial.

Common Mistakes While Taking a Home Loan:

Ignoring Processing Charges: Always compare hidden costs.

Choosing Maximum Eligibility: Borrow only what you can comfortably repay.

Ignoring Future Expenses: Account for education, healthcare, and lifestyle expenses.

Not Reading Loan Terms: Check foreclosure charges and reset clauses.

Home Loan EMI Calculator for First-Time Buyers:

First-time homebuyers should focus on:

- Affordable EMI

- Emergency savings

- Stable employment

- Low debt obligations

- Long-term affordability

Experts suggest total EMIs should not exceed 40% of monthly income.

How RBI Repo Rate Affects Home Loan EMI:

The Reserve Bank of India (RBI) changes repo rates to control inflation and economic growth.

When repo rates increase:

- Floating home loan rates increase

- EMI or tenure increases

When repo rates decrease:

- Borrowers benefit from lower interest costs

This is why floating-rate borrowers should track RBI policyannouncements.

Conclusion:

A Home Loan EMI Calculator is an essential financial planning tool for every homebuyer. It helps estimate EMIs, understand interest costs, calculate loan eligibility, compare interest rates, and plan repayment strategies effectively.

Whether you want to know:

- How much home loan you can get on ₹1 lakh salary

- Your eligibility based on income

- Joint home loan tax benefits

- Fixed vs floating interest comparison

- How extra EMIs reduce loan tenure

Using an EMI calculator can help make smarter financial decisions and save lakhs in interest over time.

Before taking a home loan, always compare lenders, understand repayment obligations, and choose an EMI that fits comfortably within your budget.

FaQ:

A Home Loan EMI Calculator is an online financial tool that helps borrowers calculate their monthly EMI based on loan amount, interest rate, and repayment tenure. It also shows total interest payable and overall repayment amount.

Home loan EMI is calculated using the standard EMI formula that considers principal amount, monthly interest rate, and loan tenure in months.

EMI = \frac{P \times R \times (1+R)^N}{((1+R)^N-1)}

A person earning ₹1 lakh per month can generally get a home loan between ₹55 lakhs and ₹70 lakhs depending on credit score, existing EMIs, age, and loan tenure.

Banks and housing finance companies offering higher eligibility often consider factors like income stability, co-applicant income, credit score, and repayment capacity. Eligibility varies from borrower to borrower.

For a ₹50 lakh home loan, lenders generally prefer a monthly income between ₹75,000 and ₹1 lakh depending on interest rate and loan tenure.

Home loan eligibility depends on:

- Property value

- Monthly income

- Existing EMIs

- Credit score

- Age

- Employment type

- Loan tenure

A Home Loan Eligibility Calculator estimates the maximum housing loan amount a borrower can qualify for based on income, liabilities, and repayment capacity.

Most banks prefer a credit score of 750 or above for faster approval and lower interest rates.

A fixed interest rate remains constant throughout the loan tenure, while a floating interest rate changes according to market conditions and RBI repo rate movements.

Floating interest rates are usually lower over long tenures, while fixed rates provide stable EMIs and predictable payments.

Yes, many lenders allow borrowers to switch between fixed and floating rates by paying a conversion fee.

The EMI depends on interest rate and tenure. For example, at 8.5% interest for 20 years, the EMI for a ₹30 lakh loan is approximately ₹26,000 per month.

Most banks offer home loan tenures up to 30 years depending on borrower age and repayment eligibility.

Yes, EMI can be reduced by:

- Transferring balance to lower-rate lenders

- Choosing longer tenure

- Negotiating lower interest rates

- Making prepayments

Yes, paying one extra EMI every year can significantly reduce loan tenure and interest burden.

Depending on loan size and interest rate, paying one additional EMI yearly may reduce tenure by 3 to 5 years.

Yes, most floating-rate home loans allow partial or full prepayment without penalties.

Borrowers can claim:

Up to ₹2 lakhs under Section 24(b) on interest payment

Up to ₹1.5 lakhs under Section 80C on principal repayment

Yes, both can claim tax benefits separately if they are co-borrowers and co-owners of the property.

A joint home loan is a housing loan taken by two or more borrowers together, usually spouses or family members.

Yes, combining incomes through a joint home loan increases overall eligibility and loan amount.

Common documents include:

- Property documents

- PAN Card

- Aadhaar Card

- Salary slips

- Bank statements

- Income tax returns

When RBI increases repo rate, floating home loan interest rates usually increase, leading to higher EMI or longer tenure.

Shorter tenure reduces total interest cost, while longer tenure reduces monthly EMI burden.

Yes, self-employed professionals and business owners can get home loans by showing stable income and financial documents.